Being examples and teaching our children how to budget is super important.

Making your money work for you is important.

We’ve spent most of our marriage struggling to climb out of debt while keeping up with too much stuff, wanting this and that – and more, more, more.

As a large military family living on one income, it’s often difficult to keep our heads above water.

We strive to teach our children the value of things and experiences. I want them prepared for real life with all its financial ups and downs.

We teach our children that a trip to Florence is more important than that new Lego set. We want them to realize that rent and food and utilities and insurance have to be paid, but sometimes we have to buy the hamburger instead of the steak to offset the expense of fixing the van. Internet and smart phones and TV are luxuries, even though we’ve come to see them as necessities, like utilities.

We have to be prepared for surprise financial setbacks with a savings account and budget in place.

Growing up as an only child, I was privy to how my parents ran our household and planned for the future. I am fortunate that I accompanied them on home and car purchases to learn how that works. They’re very organized with their investment portfolio. Since they are both retired government employees, they lived on fixed incomes, but with careful planning for many years, they live very comfortably.

Financial education is important.

Isn’t that the goal? We want to prepare for the future. We want to help jumpstart our kids into a financially successful adulthood. We want to live comfortably in retirement. We want to leave our children a legacy. We want to be able to bless others.

How do you set a budget?

Creating a budget or spending plan for the first time can be overwhelming.

A budget dictates to you what you can spend, where, and when; a spending plan allows you the control of your money every single month. It realizes that your purchases change and expenses vary from month to month and that a one-size-fits-all monthly budget doesn’t truly fit anything.

~Becoming Minimalist

What’s Your Income?

Know your income.

This should be a no-brainer, right?

Also, I know some couples who really don’t share this info with each other. That’s a warning sign and y’all should work that out.

So, know how frequently you get paid and how much.

Take into account any other income you receive and what you will use it for. Alimony, child support, investment dividends, tax returns, affiliate income, inheritance, etc. Don’t just blow that money. Have a plan for it.

I know not everyone has a set amount every pay period, with commissions or bonuses or hourly rates or whatnot…so you need to average that out to know what to expect. Then consider the lowest possibility and set your budget for that.

What are Your Bills?

Know what bills you have.

You should be organized with this, right?

We took the “no-paper option” so we get email notifications and most of our bills are automatically deducted from our accounts.

Bills are typically the ones that don’t change (or change very little) from month to month – like rent, insurance, car payments. Our utilities are in this category because they’re a set amount each month and we reconcile annually.

I also put any debt in this category. While ideally, credit cards shouldn’t be used at all or paid off monthly…we’re getting there. And I have set that payment high in order to pay it off sooner rather than later.

What are Your Expenses?

These are the extra and perhaps flexible bills each month.

Utilities often fall into this category.

Luxury items are in this category. Cable or satellite TV, Netflix, Internet, cell phones are things most people have and they sometimes fluctuate based on services used. Remember, these are not necessities. They should be the first to go during financial emergency.

Groceries and gas for vehicles. This is the most flexible area for us. I can cut costs on groceries with careful meal planning.

Our car and renter’s insurance fluctuates just a tiny bit each month, but I usually keep those items in my bills category.

We pay for music lessons for our kids.

My husband and son get their hair cut every 8 weeks or so. I cut my own hair so that’s not an expense for us.

Be honest with yourself about expenses.

Do you get your nails done weekly? Do you regularly go to the hair salon? Do you go shopping for clothes frequently? Do you need a latte fix every day?

Evaluate those expenses and put them in your budget. Consider what you might need to limit or cut out of your life to make it work.

What are Your Priorities?

Everyone has different priorities.

Some people are perfectly content to live on rice and beans and buy the latest and greatest newest technology every time a new model is released.

Others don’t have Internet or cell phones at all but have an extensive garden of fresh fruits and vegetables.

Collectors and hobbyists spend time and money on their interests.

Many want to be able to give generously.

Our priorities:

We like to travel and eat well. We’re investing for our children’s educations and our retirement. And books. Always, more books.

Because of our financial priorities, we live a little differently than a lot of people we know.

We don’t have a car payment right now. Our furniture is thrift store-yard sale chic.

We don’t go shopping for entertainment and we seldom eat out.

We opt out of ads online to limit temptation! Since we don’t have a TV, we don’t see many commercials or advertisements except on Internet sidebars and some online games or apps.

How we save money:

I try to use the library first – before purchasing books for personal use or our homeschool. Often the Kindle

The kids wear hand-me-downs from cousins, each other, thrift stores, and yard sales. I seldom buy anything new that isn’t on sale.

We don’t have huge birthdays, Christmas, Easter, or other celebrations. We prefer experiences.

Do the Math.

This is easy to create on paper or on the computer.

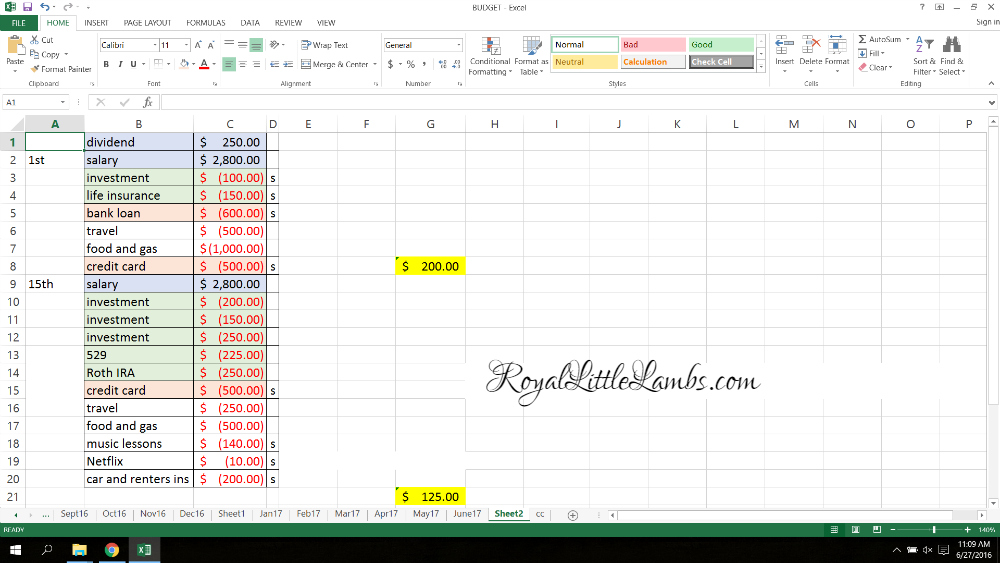

I list all our bills and income in a column on the left and amounts in the right column. I have a column for X when they’ve cleared our bank. I use an Excel spreadsheet that does the calculations for me. I have a sheet labeled for each month and a sheet for our debt so I can see our progress.

Below is an example of my current Excel

I’ve rounded the numbers and used generic names for our accounts.

I realize not everyone is in a position to invest.

I want to show you the reality.

I am not trying to brag about our income.

It’s public information anyone can look up about military service members. It’s a fixed income.

Yes, we receive some amazing benefits for being a military family: housing and utilities allowances, commissary and AAFES shopping privileges, dental and medical services at the base clinic, tax-reduced (but rationed) gasoline purchases on base. My husband’s state of residence is Illinois, so we don’t pay state taxes as a military family.

The offset is being far from home and family, missing those important holidays and events. Also, deployments, TDYs, training events, and late night or weekend exercises can be difficult on families. PCS (moving) often eats up our savings and is always stressful in many ways.

We currently have about $2500 in our savings account.

I’m fortunate to be able to stay home to educate our four children. We’re grateful for the opportunities military life offers us.

You can see we’re aggressively paying down our debt while not starving or eliminating our priority to travel. We’re still working this out with baby steps. We also have a pin and chip travel credit card that we over-used. It’s not shown in my Excel spreadsheet. We plan to attack that after these debts are paid within the year. We’re using every bit of extra income on paying that travel card (tax return, monetary gifts, and an IRA dividend we receive every autumn). We don’t plan to continue using that credit card since our new bank cards have the pin and chip now!

My Excel budget spreadsheet is color-coded.

The blue is income.

The green are investments, with amounts that seldom change.

The red is debt.

The fields left white are the flexible expenses. These amounts fluctuate from month to month.

I’m sure you noticed some gaping holes in my budget plan?

We have a separate bank account for our local expenses. Our rent, cell phones, and Internet are auto-deducted from our local account. We have a certain amount auto-deposited each pay period into the local account to cover those expenses. We use anything left over in that account each month to pay that travel credit card. We are at the mercy of the exchange rate from USD to Euro. (I love the idea of a separate account for housing expenses and I will carry that idea over when we move back to the States!)

We also have an auto deduction going directly to our church.

I have a separate account for my blogging “business.” Honestly, I don’t even sorta break even. I pour way more into this enterprise than I make every month. Some days, that’s very frustrating.

What’s Your WHY?

This goes a bit beyond just priorities.

When you get discouraged, when the van breaks down and you use your travel fund to fix it, when your child asks if you can have a “real Christmas” and you feel guilty, what will you do?

Leave room for emergencies and pray about big purchases. Obviously, a working vehicle is necessary for getting to and from work to make the money. While we cringed to fork over that $300+ for the new alternator and valves, we did so knowing that it had to be done and our trip could either be postponed or we could be more frugal somewhere else.

We remind ourselves what the big picture is: planning for our futures, teaching our children values, and leaving a legacy for our kids.

Sure, we splurge sometimes on gelato, a cute new shirt or shoes in sale when needed, flowers for the garden or dining table for a special occasion, or that Kylo Ren lightsaber

We try to make sure there’s room in the budget for fun or it becomes drudgery.

UPDATE 8/25/16: We have PAID OFF TWO accounts! Only 3 to go. We plan to have those paid by May!

Update August 2017: Only 1 account left to go!

Resources:

- Debt-Proof Living: How to Get Out of Debt & Stay That Way by Mary Hunt

- 31 Days to Radically Reduce Your Expenses: Less Stress. More Savings by Kalyn Brooke

- Slaying the Debt Dragon: How One Family Conquered Their Money Monster and Found an Inspired Happily Ever After by Cherie Lowe

- 31 Days of Living Well and Spending Zero: Freeze Your Spending. Change Your Life. by Ruth Soukup

- Unstuffed: Decluttering Your Home, Mind, and Soul by Ruth Soukup

- Clutter Free: Quick and Easy Steps to Simplifying Your Space by Kathi Lipp

- The Spender’s Guide to Debt-Free Living: How a Spending Fast Helped Me Get from Broke to Badass in Record Time by Anna Newell Jones

- The Year without a Purchase: One Family’s Quest to Stop Shopping and Start Connecting by Scott Dannemiller

- The Year of Less: How I Stopped Shopping, Gave Away My Belongings, and Discovered Life is Worth More Than Anything You Can Buy in a Store by Cait Flanders

- Make Room for What You Love: Your Essential Guide to Organizing and Simplifying by Melissa Michaels

Do you have any budget tips to share?

You might also like:

This is a good breakdown on how to create a budget. It’s always a good thing to have one, but if someone doesn’t know where to start, it can be daunting!

These are all great ideas. I need to be better at setting up a budget. I would love to have you join us at Family Joy Blog Link Up Party this week. Check us out http://thinking-outside-the-pot.com/?p=2711

This is sooo important and so frequently overlooked. I especially liked the point about being honest with yourself. I have written about times when I have heard friends complain about money problems while they eat lunch out daily. It is important to live within your means and to know what you can really afford. Great post!

I agree with you when it comes to the library. Once a year when the kids have a day off, we do go to the book store. This is a fun trip, and we can give the kids thier budget. A great learning tool and the kids get some books to take home.

Great post! Such helpful and useful tips on budgeting. Thanks so much for sharing, Love! GOD bless you! :-)

Excellent read!!

You really break this budgeting thing down so well! It’s so important to discuss priorities with your spouse. That’s a huge area of disagreement (at least with us sometimes). Thanks for these guidelines. Pinning!

Great tips! Sometimes just getting started with a budget is the hardest part. You have made it less daunting to at least get started. Thank you for sharing on Family Joy Blog Link-up Party. Hope you are having a great week!

Love these tips! Pinned to share. Thanks so much for sharing with us this week at Brag About It!

Great tips and I love that you show exactly how you do yours with the spreadsheet etc.

Great tips! And I must agree, books are a priority on the budget :)

Thank you for sharing this week at the Art of Home-Making Mondays at Strangers & Pilgrims on Earth! :)

Very good, Jennifer. My tip – don’t be an In The Dark Dorothy or In The Dark Dan – couples need to know everything about the budget whether they are the one making out the bills or not. A good friend of mine woke up one morning with a huge mess on her hands when her husband walked out on her. She had no clue to what he was doing with the money. She found they were 100’s of thousands of dollars in debt and wasn’t paying any of it. It pays to be knowledgeable of the finances in a home.

Thanks for sharing with Thankful Thursdays.

I absolutely agree! So tragic when communication doesn’t happen. I’ve known couples like that too.

This looks very practical and helpful! Thanks for sharing. I’m sure most of us could do better in this area! Blessings!

This is comprehensive and really lays it all out there! Years ago, my husband and I took a Crown Financial class that forced us to talk about money. It was so uncomfortable but so necessary!

I LOVE Crown Financial. I used to teach those classes to single moms!

This is an important skill to learn. Everyone needs to know how to do this. I don’t see how anyone survives without doing it.

Thank you for sharing this with us on the #HomeMattersParty. We hope to see you when we open our doors at 12AM EST on Fridays.

What a great, detailed and important post. Budgeting can really set you free financially. Thanks for sharing with #EverythingKids. I think this is a critical process for families.

Thanks for sharing on Let’s Get Real Friday. You have great tips and my husband and I did it for years. We now do it less formally because of the years of experience we have. One of the best things we did was to make sure we always saved money, even it if was a few dollars. It grows over time and can make a difference in being in debt or debt free.

Thanks for sharing this at Booknificent Thursday on Mommynificent.com! It’s really helpful.

Tina

Figuring out what’s important and why is a great motivator to budget. Thanks for sharing at the Healthy Living Link Party!

Blessings, Leigh